Introduction to GloBE: Scope, Thresholds, and the EUR 750m Test

Amith R

Overview

This video introduces Pillar Two of the OECD's global tax regulations, focusing on the 15% minimum corporate tax. It explains the historical context, detailing how globalization and digitalization created loopholes that allowed multinational enterprises (MNEs) to shift profits to low-tax jurisdictions, leading to a 'race to the bottom' in corporate tax rates. Pillar Two aims to address these issues by ensuring MNEs pay a minimum effective tax rate of 15% regardless of where they operate. The video outlines the scope of Pillar Two, specifically the consolidated revenue threshold of €750 million, and discusses how to apply this threshold, including currency conversions, look-back periods, and treatment of mergers, acquisitions, and disposals. It emphasizes the importance of understanding the OECD Model Rules and Commentary for effective application.

Save this permanently with flashcards, quizzes, and AI chat

Chapters

- Traditional international tax rules, based on physical presence (permanent establishment), are insufficient in a digitalized global economy.

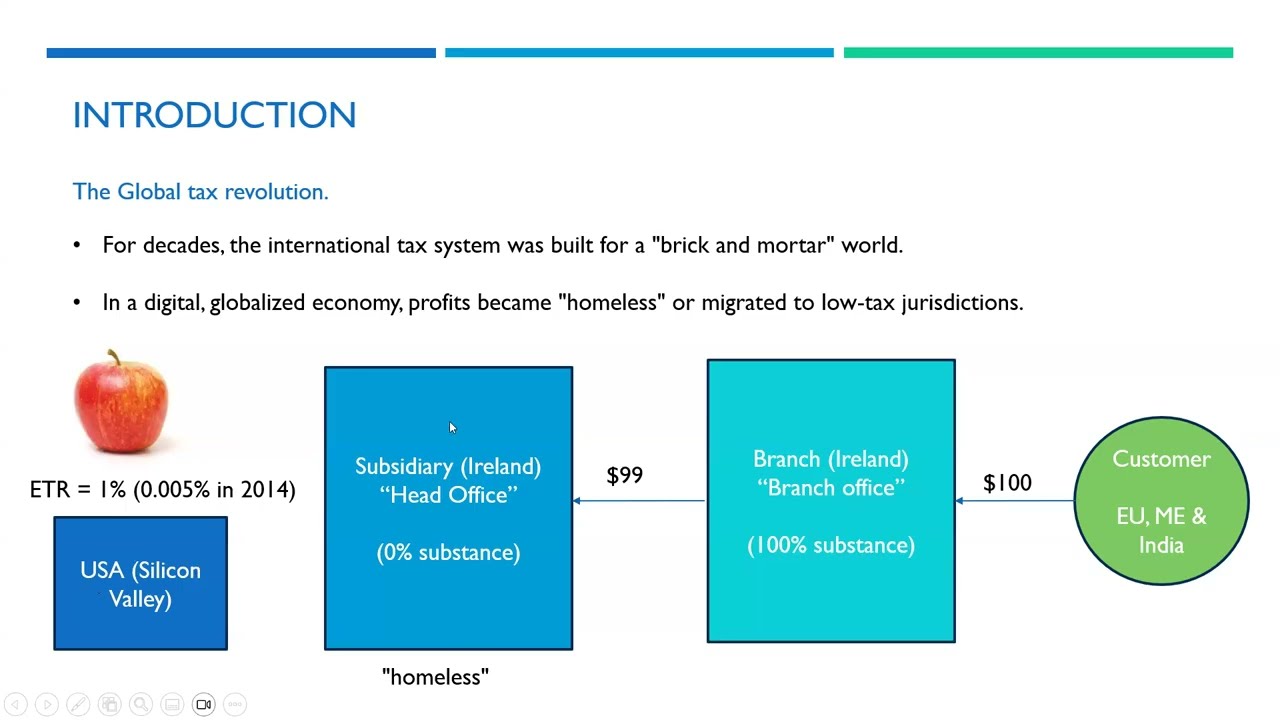

- MNEs exploit loopholes to shift profits to low-tax jurisdictions, leading to 'homeless' profits and reduced tax revenue for market countries.

- The 'race to the bottom' has driven down corporate tax rates globally, impacting public services and creating an uneven playing field.

- The COVID-19 pandemic highlighted the need for governments to have sufficient funds for public services, accelerating the push for global tax reform.

- Pillar Two introduces a global minimum effective tax rate of 15% for large MNEs.

- This aims to ensure that MNEs pay a minimum level of tax on their profits, regardless of their location or tax planning strategies.

- Pillar One, focusing on digital services tax and profit allocation, is still under development and faces significant challenges.

- Pillar Two is considered more flexible and has been adopted by over 140 countries.

- Pillar Two applies to MNE groups with consolidated annual revenues of €750 million or more.

- This threshold must be met in at least two of the four fiscal years immediately preceding the tested fiscal year.

- The €750 million threshold aligns with Country-by-Country Reporting (CbCR) requirements to minimize additional compliance burdens.

- The 'two out of four years' rule prevents MNEs from oscillating in and out of scope due to single-year fluctuations or one-off events.

- Revenue is determined based on audited consolidated financial statements, using IFRS 15 (or equivalent for US GAAP) for the revenue line.

- Amounts must be converted to Euros using the average exchange rate for the relevant fiscal year, with a hierarchy of sources for exchange rates (ECB, central bank, etc.).

- For groups with less than four years of history, the test applies to the years that exist.

- For newly formed groups or mergers, the combined historical revenues of predecessor groups are considered.

- For acquisitions or disposals during the look-back period, revenue is included only from the date of acquisition or up to the date of disposal, without annualization.

- Effective study of Pillar Two requires understanding both the OECD Model Rules and the extensive Commentary.

- Key documents for compliance include audited consolidated financial statements, revenue extraction working papers, and exchange rate documentation.

- A formal assessment conclusion memo should record the determination of scope and the rationale.

- Annual reviews and retention of documentation for at least seven years are mandatory.

Key takeaways

- Pillar Two was developed to address profit shifting and tax competition exacerbated by digitalization and globalization.

- The core of Pillar Two is a 15% global minimum effective tax rate for large MNEs.

- An MNE group must have consolidated revenues exceeding €750 million in at least two of the four preceding years to be within the scope of Pillar Two.

- Revenue recognition for the threshold test follows accounting standards like IFRS 15, with specific rules for currency conversion and treatment of corporate events.

- The 'two out of four years' rule is designed to ensure stability in scope determination and avoid fluctuations.

- Proper documentation, including financial statements and detailed working papers, is critical for compliance and audit purposes.

- Understanding the OECD Model Rules and their accompanying Commentary is essential for interpreting and applying Pillar Two.

Key terms

Test your understanding

- What were the primary drivers that necessitated the introduction of Pillar Two?

- How does the €750 million revenue threshold determine if an MNE group is subject to Pillar Two rules?

- Explain the rationale behind using a 'two out of four years' look-back period for the revenue threshold.

- What are the key considerations when converting revenues from local currencies to Euros for the threshold test?

- How do mergers, acquisitions, and disposals impact the calculation of consolidated revenue for Pillar Two scope determination?