13:23

Options Flow: The Edge You've Been Looking For

Aleks Rosme

Overview

This video explains how options flow, specifically the hedging activities of market makers (dealers), drives price movements in futures markets like NQ and ES. Instead of focusing on traditional technical analysis or market psychology, the video argues that understanding the 'Greeks' (Delta, Gamma, Vanna, Charm) and how dealers dynamically hedge their option positions provides a significant trading edge. By analyzing these mechanics, traders can better anticipate market behavior, whether it's range-bound consolidation or accelerated trends, leading to more consistent profitability.

How was this?

Save this permanently with flashcards, quizzes, and AI chat

Chapters

- Traditional technical analysis methods like drawing lines and boxes on charts are ineffective for consistent profitability.

- The concept of 'liquidity' as taught by many influencers is misleading and not used by institutional traders.

- True market movement is driven by a specific market mechanic: options flow and the resulting dealer hedging.

- Market makers (dealers) who provide liquidity for index options must hedge their positions in the underlying futures markets (like NQ and ES).

This chapter challenges common trading beliefs and introduces the core concept that understanding dealer hedging, not just price action, is crucial for developing a profitable trading strategy.

The speaker contrasts ineffective chart drawing with the underlying mechanic of dealer hedging in options.

- When traders buy options (e.g., a call), the dealer who sold it takes on risk.

- Dealers aim to remain 'delta neutral,' meaning they don't want to profit or lose from price direction.

- To offset the risk from selling a call (which creates negative delta), dealers buy futures.

- Conversely, when dealers sell a put (creating positive delta), they sell futures to hedge.

- This constant, mechanical hedging by dealers in response to options trades is what actually moves the futures market.

This explains the fundamental reason why futures prices move: it's not random, but a direct consequence of market makers balancing their risk from options trades.

When a trader buys a call option, the dealer who sold it immediately buys NQ futures to hedge their resulting negative delta.

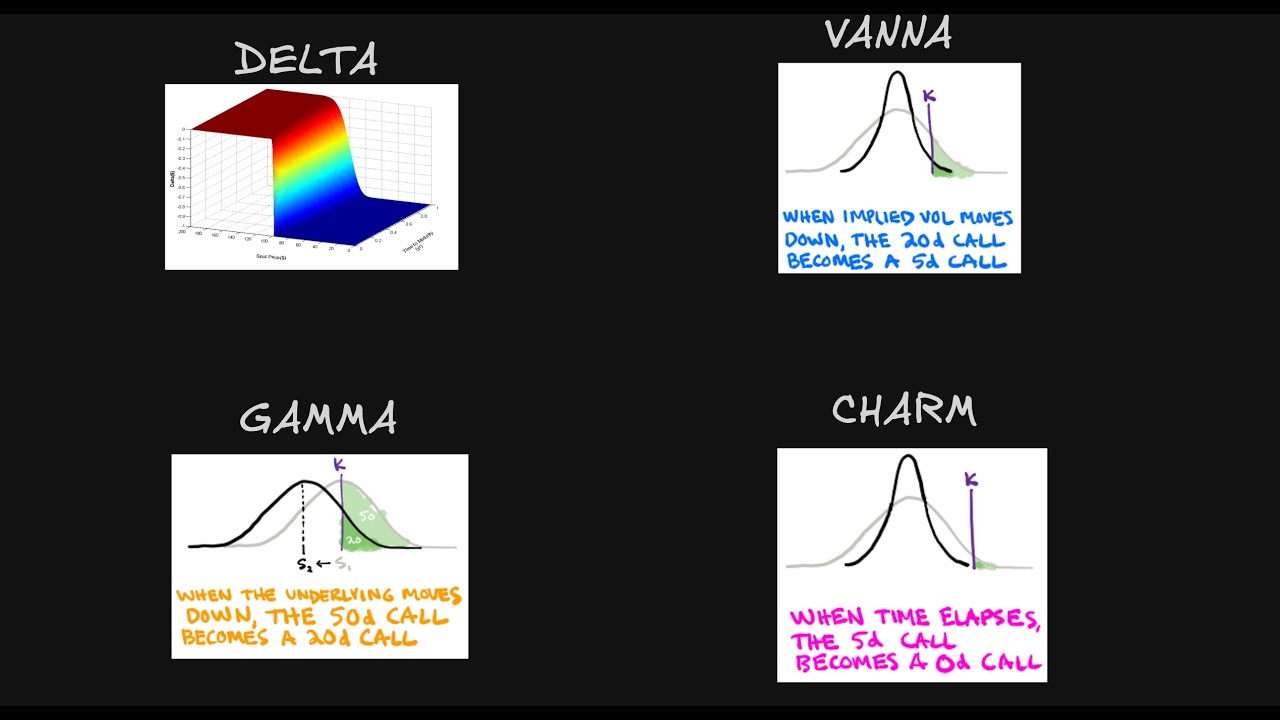

- Gamma measures the rate of change of an option's delta as the underlying price moves.

- Dealers constantly adjust their delta hedges due to gamma, which can either stabilize or accelerate price movements.

- When dealers are 'long gamma' (positive gamma), they buy when price falls and sell when price rises, creating a mean-reverting, range-bound market.

- When dealers are 'short gamma' (negative gamma), they buy when price rises and sell when price falls, amplifying the move and leading to strong trends.

- Positive gamma environments often result in tight ranges and failed breakouts, while negative gamma leads to aggressive price acceleration.

Understanding whether dealers are long or short gamma allows traders to anticipate whether the market will likely consolidate or trend aggressively, informing their trading approach.

In a positive gamma environment, if NQ moves up, dealers sell futures to re-hedge, pushing NQ back down, creating a 'rubber band' effect.

- Vanna describes how dealer hedging changes when implied volatility (like the VIX) moves.

- When VIX drops, dealers are forced to buy futures; when VIX rises, they are forced to sell futures.

- This Vanna effect can cause markets to drift higher or lower without obvious news, as dealers mechanically adjust hedges based on VIX changes.

- Charm relates to the slow directional drift caused by options losing delta purely due to time decay (theta) as the day progresses.

- Charm's effect is most noticeable in the afternoon, pulling prices towards significant levels, but is less impactful in the morning trading session.

Vanna and Charm explain subtle market movements that aren't immediately obvious on charts or order flow, providing additional context for price action, especially the Vanna effect which can be unseen.

A market might slowly drift higher after a VIX spike and subsequent drop, because dealers are mechanically buying futures due to Vanna as the VIX declines.

- The four Greeks (Delta, Gamma, Vanna, Charm) represent distinct forces influencing market behavior.

- Delta shows current hedging direction, Gamma indicates trend acceleration or stabilization, Vanna relates to volatility shifts, and Charm explains time decay effects.

- The key to profitability is not specific entry signals, but understanding the dominant force driving the market on any given day.

- This framework provides essential market context, differentiating consistently profitable traders from others.

This chapter synthesizes the concepts, emphasizing that a deep understanding of these underlying mechanics provides the crucial market context needed for strategic trading decisions.

Before trading, a trader should ask: 'Which of these forces (Delta, Gamma, Vanna, Charm) is dominant today?' to set their trading bias.

Key takeaways

- Market makers (dealers) are the primary drivers of futures price movements through their options hedging activities.

- Understanding dealer hedging mechanics, particularly the 'Greeks,' provides a significant trading edge over traditional technical analysis.

- Gamma dictates whether the market will trend aggressively (short gamma) or remain range-bound (long gamma).

- Vanna explains how changes in volatility (VIX) force dealers into mechanical buying or selling of futures, influencing price direction.

- Charm describes the slow, time-decay-driven drift in prices, particularly in the afternoon.

- The most profitable traders use this framework to understand market context rather than relying solely on price action or psychology.

- Consistently profitable trading comes from understanding the dominant market mechanic for the day, not from finding perfect entry signals.

Key terms

Options FlowMarket Maker (Dealer)HedgingDelta NeutralDeltaGammaVannaCharmFutures Market (NQ, ES)Implied Volatility (VIX)

Test your understanding

- How does a market maker's need to remain delta neutral influence futures price movements?

- What is the difference in market behavior between a 'long gamma' and a 'short gamma' environment for dealers?

- How does a change in the VIX (Volatility Index) mechanically affect futures prices according to the Vanna effect?

- Why is understanding the 'Greeks' considered more important for profitability than traditional chart patterns?

- How does the Charm effect contribute to price movement, and when is it most relevant for traders?