Activity Based Costing (with full-length example)

Edspira

Overview

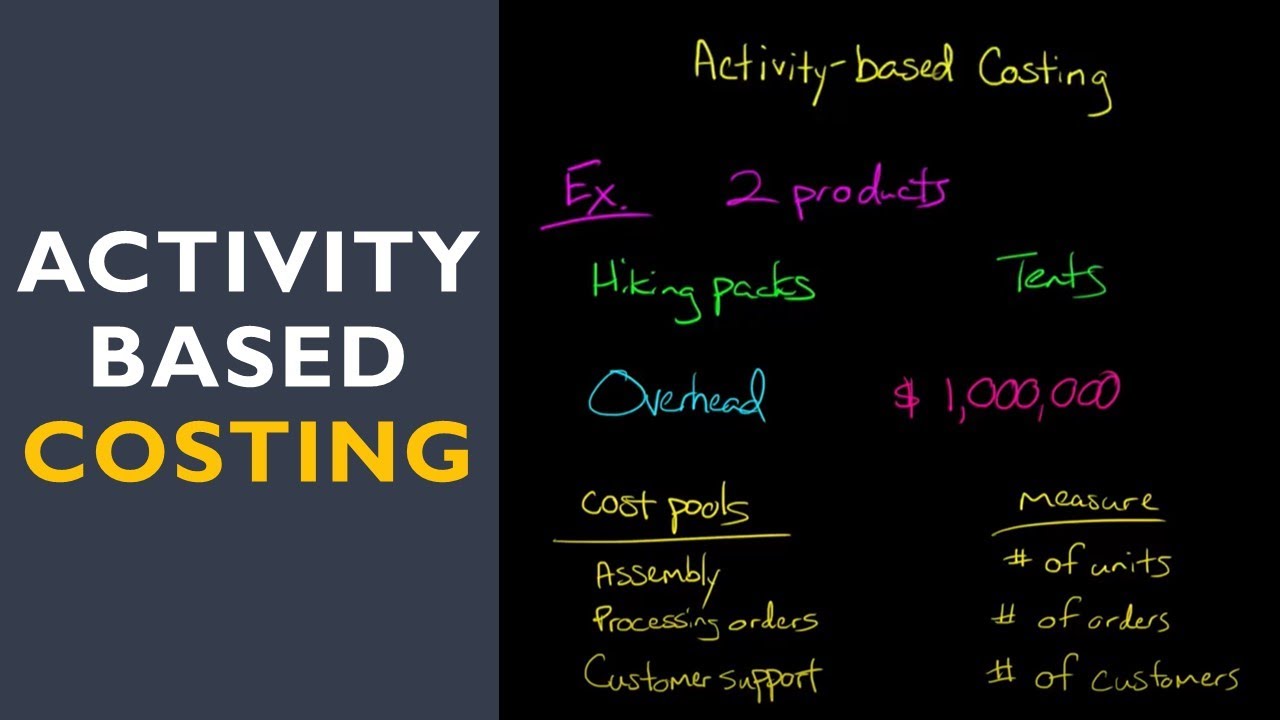

This video explains Activity-Based Costing (ABC) as a more precise method for allocating non-direct costs (overhead) to products compared to traditional methods like using machine hours or labor hours. It details a step-by-step process for implementing ABC, including identifying activities and cost pools, assigning overhead to these pools, calculating activity rates, and finally, applying these rates to cost objects (products) to determine their true cost. The example contrasts the costs of producing hiking packs and tents, highlighting how different activities and their drivers (like number of orders or customers) can lead to significantly different overhead allocations even for products with the same production volume.

Save this permanently with flashcards, quizzes, and AI chat

Chapters

- Traditional costing methods struggle to accurately allocate non-direct costs (overhead) to products.

- Direct costs (materials, labor) are easily traceable, but overhead is not.

- ABC is a more precise method for allocating overhead by identifying specific activities that drive costs.

- ABC requires more information and is more complex to implement than traditional methods.

- The first step is to identify the specific activities that consume overhead resources.

- These activities are grouped into 'cost pools' (e.g., assembly, order processing, customer support).

- Each cost pool needs a 'cost driver' – a measure of how much the activity is used (e.g., number of units, number of orders, number of customers).

- Some costs, like factory rent ('other' category), may not be directly assigned to products if they are organization-sustaining.

- The total overhead cost is estimated and then allocated to the identified cost pools.

- This allocation is often based on interviews with employees to determine the percentage of time or resources spent on each activity.

- The 'other' category, for organization-sustaining costs, is not allocated to products in this model.

- For each cost pool, an 'activity rate' is calculated by dividing the total cost in the pool by the total amount of its cost driver.

- This rate represents the cost per unit of the activity driver.

- Multiple activity rates are generated, unlike traditional single plant-wide rates.

- The calculated activity rates are used to assign overhead costs to specific products (cost objects).

- This involves multiplying the activity rate by the actual amount of the cost driver consumed by each product.

- ABC reveals that products consuming more of certain high-cost activities (like order processing or customer support) will be allocated more overhead, even if production volumes are similar.

- The sum of allocated overhead to products may not equal the total overhead if an 'other' category was excluded.

Key takeaways

- Activity-Based Costing (ABC) improves overhead allocation accuracy by linking costs to specific activities.

- Traditional costing methods often over-allocate or under-allocate overhead due to their reliance on single, broad cost drivers.

- Identifying relevant activities and their cost drivers is the foundation of an effective ABC system.

- Employee input is vital for accurately assigning overhead to cost pools.

- ABC generates multiple activity rates, reflecting the diverse drivers of overhead costs.

- Products that consume more high-cost activities will bear a higher overhead allocation, regardless of production volume.

- ABC provides better information for decision-making, such as pricing, product mix, and process improvement.

Key terms

Test your understanding

- What is the primary limitation of traditional costing methods that ABC aims to address?

- How does Activity-Based Costing differ from traditional methods in its approach to allocating overhead?

- What are the key steps involved in implementing an Activity-Based Costing system?

- Why is it important to identify specific cost drivers for each activity pool in ABC?

- How can ABC lead to different cost conclusions for products that are produced in similar volumes?